3I0-012 Online Practice Questions and Answers

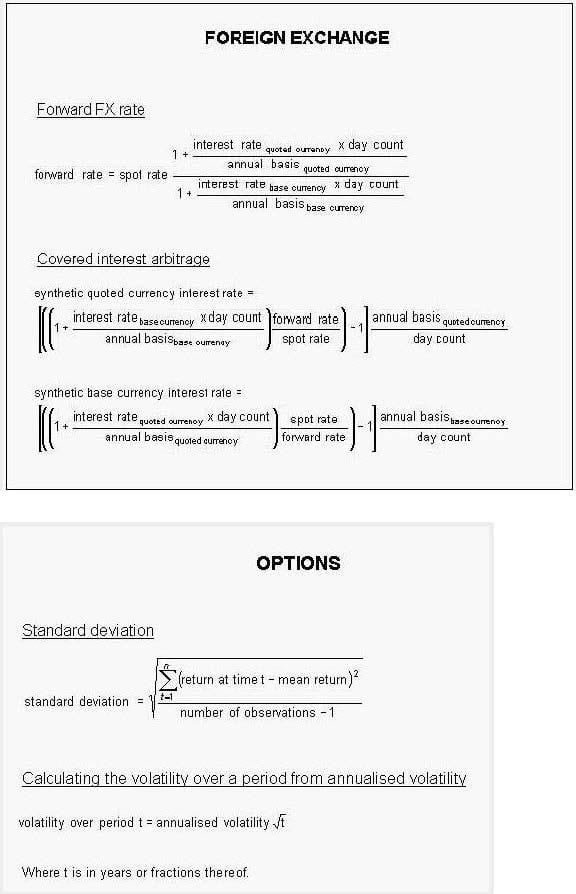

EUR/USD is 1.3080-83 and EUR/CHF is 1.2160-63. What price would you quote to a customer who wishes to sell CHF against USD?

A. 1.0759

B. 0.9299

C. 1.5909

D. 0.9295

What is a short straddle option strategy?

A. A long call option + long put option with the same strike prices

B. A short call option + short put option with the same strike prices

C. A long call option + short put option with the same strike prices

D. A short call option + long put option with the same strike prices

VaR increases with:

A. lower correlation of underlying risk factors

B. a shorter time horizon

C. a lower confidence level

D. a higher confidence level

Repo is said to have "double indemnity" due to the creditworthiness of the counterparty and:

A. A written legal agreement between the parties

B. The oversight of the transaction by the custodian of the collateral

C. The creditworthiness of the collateral

D. The right of close-out and set-off in an event of default

For which one of the following disputes is the Chairman and members of the ACI's CFP ready to assist through the ACI's Expert Determination?

A. all legal disputes

B. disputes related to market practice or conduct as set out in the Model Code or in any other Code of Conduct

C. disputes between two market participants, at least one of them being a member of ACI

D. disputes related to over-the-counter financial instruments as detailed in appendix four of the Model Code

You have bought a 93-day US Treasury bill at 5.63%. What is the true yield?

A. 5.71%

B. 5.69%

C. 5.72%

D. 5.62%

How much is one big figure worth per million of base currency if EUR/GBP is 0.8990?

A. GBP 10,000.00

B. EUR 10,000.00

C. GBP 8,990.00

D. EUR 8,990.00

The delta of an `at-the-money' long call option is:

A. Between +0.5 and +1

B. +0.5

C. Between 0 and +0.5

D. Zero

How can options be used to synthesize a short position in the underlying commodity?

A. A short put option + long call option at the same strike price

B. A long put option + short call option at the same strike price

C. A short put option + short call option at the same strike price

D. A long put option + long call option at the same strike price

How many USD would you have to invest at 3.5% to be repaid USD125 million (principal plus interest) in 30 days?

A. USD 124,641,442.43

B. USD 124,636,476.94

C. USD 124,635,416.67

D. USD 123,915,737.30